How I used Koyfin to learn about Consumer Staples

I tend to ask a lot of questions. If my Mother was alive, she’d tell you, that she raised me to be this way. I was inquisitive as a kid because I didn’t like being told to accept answers that didn’t make sense in my head. My Mother used to get frustrated with it until she understood I was asking questions about those answers so that I could learn for myself.

After that lightbulb moment, she encouraged me to speak my mind, and ask more questions.

Thus when it comes to investing, I am the same way. I am constantly trying to figure out why something works and even more so, why doesn’t something work.

Recently, I signed up for an account on Koyfin and quite, honestly I’ve been like a kid in the candy store.

Koyfin via its multiple data sources and analytics capabilities allows me to ask A LOT of questions and go searching for answers all in one spot. To say its been awesome, would be an understatement.

So that brings us to today…

While playing with a stock screener, I came across a ticker (Dollarama DOL 0.00%↑ ) I had never heard of that has had a tremendous return over the last 10 years. Honestly I was thoroughly impressed.

This led to some additional questions, such as…

What is this company?

What exchange does it trade on?

What companies are similar?

What does the balance sheet look like?

Again, Koyfin came to my rescue and suggested some similar companies one of which (Five Below FIVE 0.00%↑ ) I am all too familiar with because my kids love spending money there.

I spent time comparing the two companies, then added Dollar General DG 0.00%↑ to the mix and realized, I missed something in the last couple of years that was right in front of me...

In fact, I mentioned my thoughts on twitter and got the following response from the Koyfin account:

Seeing that tweet, made me feel like an idiot. After reading everything I could on Warren Buffet the past few years, this was an obvious observation. Like everyone else I didn’t pay attention to it.

The question is why? Likely because it’s boring everyday stuff that we take for granted.

Consumer staples according to Investopedia, are “companies that create products considered essential by consumers. This category includes things like foods and beverages, household goods, and hygiene products as well as alcohol and tobacco.”

i.e. it’s the stuff we use everyday.

Buffet likes boring and consumer staples are exactly that. My investing journey started with Buffet so consume staples has piqued my interest.

In my opinion, one of the best places to start to learn about a sector is examining a sector specific index fund.

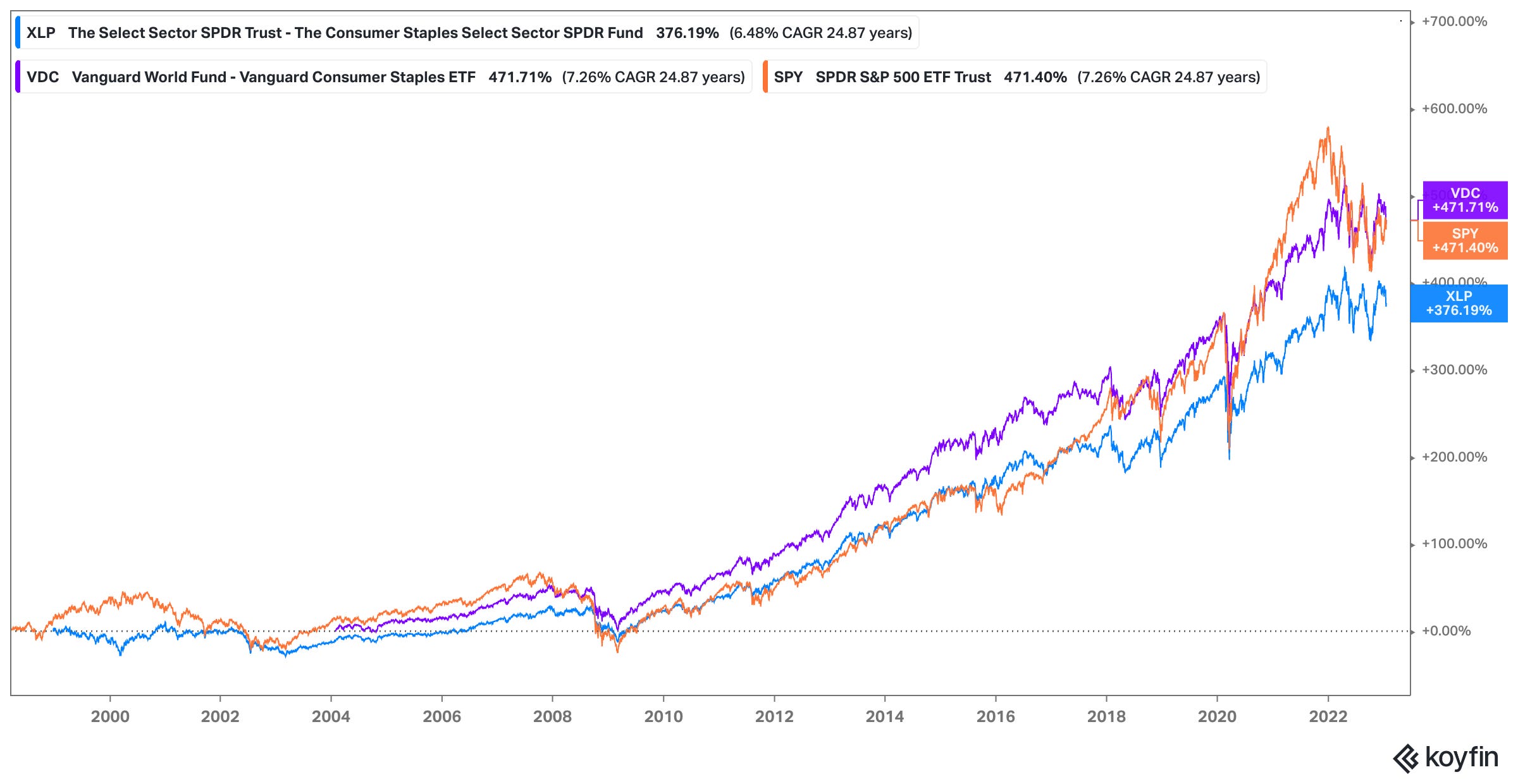

XLP 0.00%↑ and VDC 0.00%↑ are the two I chose to look at. To get a broad snapshot of the two funds I used VettaFi, which is a great site to research ETFs.

One of the first things you’ll notice is that these funds have similar characteristics, however differ in their number of holdings, what indices they are tracking, and have different return profiles over the last 20 years.

SPY 0.00%↑ is listed on the chart as a reference point because its a popular S&P 500 ETF that most people would know. Its also important to point out Consumer Staples are roughly 6.2% of the S&P 500 index vs the other two funds which only care about matching their respective consumer staples indices.

The chart shows these funds follow a similar path but theres some type of underlying difference. The question is what is it?

Using the tool provided by the ETF Research Center you’ll see that 100% of the holdings in $XLP are contained in $VDC. Thus its easy to infer there are likely a number of securities in the sector that generated the difference in the performance between these two.

So what are the characteristics that define the consumer staple sector?

Being the degenerate that I am, I personally love value investing, so lets just start with some classic metrics, like price-to-earnings (P/E), price-to-book (P/B), and debt-to-earnings, which are some of my favorite things to look at when comparing securities in a single sector.

The consumer staples sector on a whole has the following characteristics (screenshot from Fidelity):

These metrics (fundamentals) look at the sector as a whole. Thus they are averages. The mathematical part of my brain tells me that if I am looking for something that is undervalued by the market, I should look for Consumer Staple companies with a P/E less than 23 but with similar characteristics to the rest of the sector.

The results of running that criteria (along with Total Debt / Equity < 121.95) generated a list of 51 names to look into.

Overall, I’d say thats pretty cool.

But this also took a lot of work and time.

Personally I love investing, but I am a realist. Not everyone wants to spend time looking into this stuff, which is why I think taking the index approach is the correct approach, if you aren’t willing to put the time into figuring out what companies to invest in based upon your own criteria.

99% of the stuff that is out there on the internet with respect to investing, doesn’t need to be learned unless you truly love this stuff (hint: I do).

As always if you have questions or concerns regarding creating an emergency fund, investing, real estate, insurance, or planning for the future, don’t be afraid to speak with a qualified financial advisor. Smart Asset has a great tool to find an advisor in your area or feel free to email me (contact@surgifi.com) to help you on your path to financial independence.

In the recent P&G earnings call, the company mentioned that their costs were increasing and, unlike during 2021 and early 2022, they are not able to fully pass on the increasing costs to their customers due to the customers' increasing debt levels and lack of access to credit (see Discover Financial earnings call). As the costs might continue to increase and not be fully passed on to customers, I am having difficulty understanding the rationale for a P/E of 23 for this sector at a time when short-term treasuries are paying >4%. However, I have made many investment mistakes in the past. Why am I wrong?

Great rationale, great take … thank you